Navigating the institutional business loan application process in India can be challenging for many entrepreneurs. Borrowers often face delays, higher interest rates, or rejection due to disorganized financial records, poor credit planning, or a lack of understanding of lender requirements. Understanding how to systematically prepare an application and align with credit underwriter standards is essential to securing funding on competitive terms.

Credit Score Optimization and Pre-Application Steps

Before submitting a formal loan application, borrowers must evaluate and optimize their credit standing :

- Review Credit Reports: Lenders rely heavily on the TransUnion CIBIL score to assess repayment discipline. Promoters should review their credit files to ensure accuracy and resolve any discrepancies.

- Target Ideal Benchmarks: A personal and corporate CIBIL score of $\ge 750$ is ideal for securing competitive rates. If a score is low, borrowers should focus on paying EMIs on time, maintaining low credit utilization, and avoiding multiple concurrent loan applications.

- Define Borrowing Needs: Borrowers must identify their specific funding requirements and match them to the appropriate credit instrument, such as term loans, working capital limits, or equipment financing.

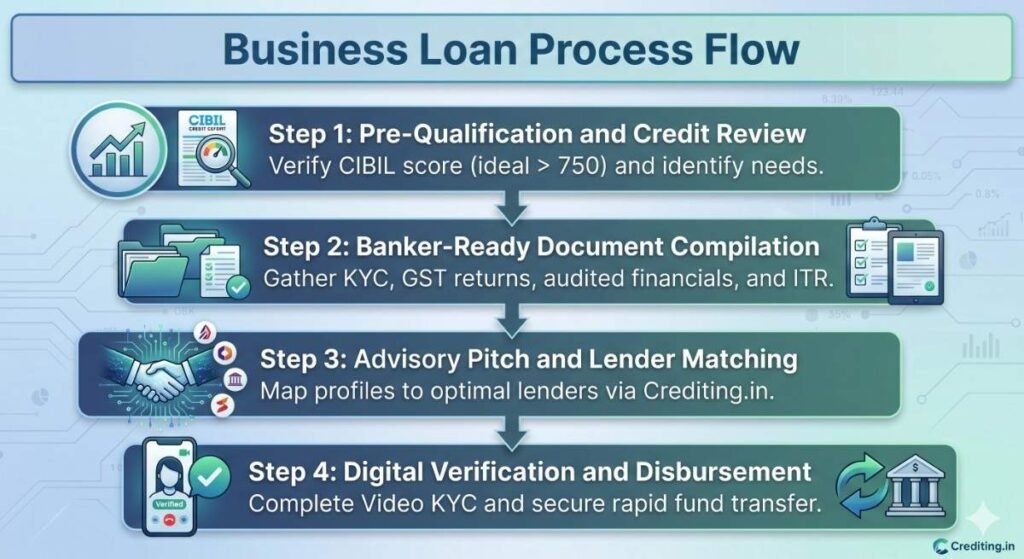

Step-by-Step Credit Application and Approval Guide

Following a structured process helps ensure a smooth credit approval journey :

- Strategic Alignment: Borrowers must establish a clear business vintage of at least two to three years and verify that their monthly and annual sales meet lender benchmarks (such as a minimum monthly sales of ₹2 Lakh).

- Document Compilation: Gathering all mandatory financial, tax, and registration documents upfront prevents processing delays.

- Lender Matching: Submitting the application through a specialized advisor like Crediting.in allows borrowers to map their profiles to the optimal lender, avoiding multiple hard inquiries that can damage credit scores.

- Verification and Disbursement: After receiving a digital sanction letter, borrowers complete Video KYC (V-KYC), e-sign the loan agreement, and secure rapid fund transfer.

The Banker-Ready Document Portfolio Checklist

A complete and organized document portfolio is key to a smooth underwriting process :

Document Category | Target Mandatory Items | Specific Underwriting Purpose |

Identification & Legality | PAN, Aadhaar, Partnership Deed/MoA, Incorporation Certificate | Confirms identity and legal borrowing authorization |

Revenue Verification | GST Returns (Last 4 Quarters) | Validates actual sales trends and operational activity |

Tax & Solvency Proof | Audited ITR & Balance Sheets (3 Years) | Assesses financial capacity, tax compliance, and net worth |

Cash Flow Statements | 12-month current account PDFs | Monitors check bounces, operational cash flow, and average balances |