Securing a business acquisition loan in India is one of the most complex corporate finance transactions an entrepreneur can undertake. Starting a business from scratch carries significant operational and market risks. Conversely, acquiring an established target company with a verified customer base, functioning infrastructure, and consistent historical cash flows is a highly effective scaling strategy.

However, because business acquisitions involve substantial capital, complex legal transitions, and unique regulatory limitations, securing the right debt structure is essential to preventing financial friction post-acquisition

The Regulatory Challenge and the Share Purchase Financing Trap

The primary structural obstacle in Indian acquisition financing is the restrictive banking environment governed by the Reserve Bank of India (RBI). Under current guidelines, domestic commercial banks are generally prohibited from extending loans to purchase shares or equity in domestic target companies. This framework is designed to prevent speculative leveraging and protect depositors from equity market volatility.

To bridge this regulatory gap, experienced debt advisors structure acquisitions through alternative lending channels :

- NBFCs & Credit Funds: Non-Banking Financial Companies and Alternative Investment Funds (AIFs) are not bound by the same share-purchase lending restrictions. They can extend high-value credit backed by a pledge of target shares and charges on operating assets.

- Foreign Debt & FDI SPVs: For international buyers acquiring an Indian target, domestic banks cannot participate. In such cases, advisors establish an offshore Special Purpose Vehicle (SPV) that raises foreign capital, which is then routed into India as Foreign Direct Investment (FDI).

- Structured Debt Instruments: Acquisitions are frequently funded by issuing Non-Convertible Debentures (NCDs) or structured mezzanine capital. These instruments combine the stability of debt with flexible exit options at predefined intervals.

Types of Loan facility

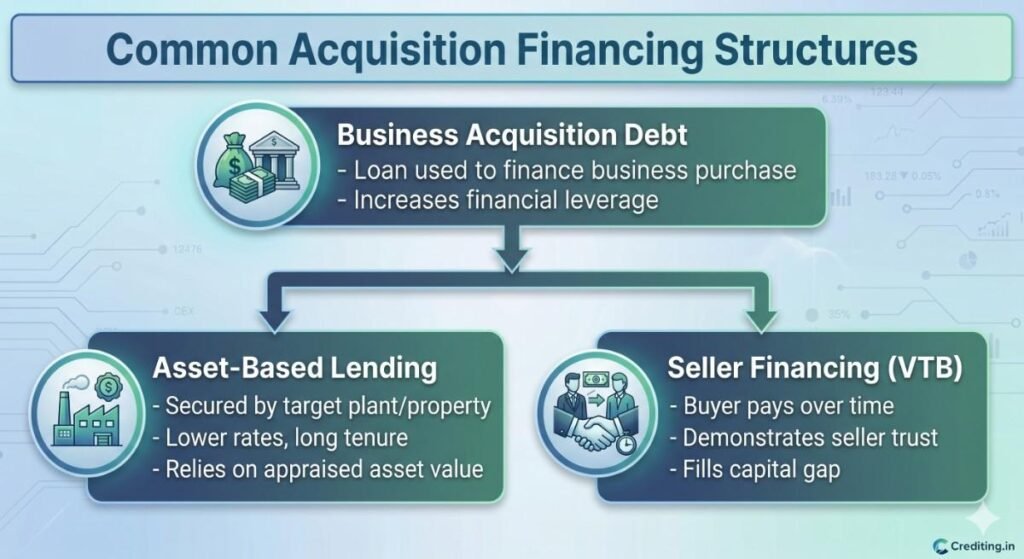

- Asset-Backed Term Loans: If the target company owns substantial tangible assets (e.g., real estate, advanced manufacturing plant, or machinery), commercial lenders can extend a secured term loan based on the appraised market value of those assets.

- Seller Financing: In this highly cooperative structure, the seller agrees to receive a portion of the purchase price in structured installments over a multi-year period. This acts as deferred debt, aligning the seller’s interests with the smooth transition of operations.

- Bridge Loans: Because corporate transactions require speed, bridge loans are short-term facilities (usually 6 to 12 months) that provide immediate capital to close the deal while long-term debt or equity structures are finalized.

Underwriting Metrics for Acquisition Debt

Lenders do not risk capital on a transaction without analyzing both the buyer’s operational experience and the target’s financial health.

Parameter | Target Standard Metric | Verification Requirement |

Buyer Vintage | 3 Years of successful management history | Promoter profiles, MoA, and experience proofs |

Target Turnover | Minimum ₹40 Lakhs to ₹20 Crore+ p.a. | Audited Balance Sheet and P&L for last 3 years |

Valuation Feasibility | Independent Asset & Equity Valuation Report | Detailed valuation certified by registered valuer |

Target DSCR | Projected DSCR 1.25 post-leverage | 5-year financial projections and business plan |

Transaction Legality | Clear and enforceable acquisition terms | Letter of Intent (LoI) & Share Purchase Agreement |